The journey to a successful retirement involves many years of disciplined saving and investing. As you stand on the threshold of a well-deserved indefinite vacation, one crucial challenge remains: How can you ensure that your savings will last your whole lifetime?

Navigating retirement distributions can feel like walking a tightrope. Withdraw too much, and you risk your nest egg running out. Withdraw too little, and you won’t be able to enjoy the quality of life you desire. Often, retirees end up adopting a static plan that is too conservative — or worse, too reckless.

The most common retirement distribution strategies involve consistently withdrawing some fixed percentage or dollar amount from your portfolio, similar to the hypothetical scenario below. While this approach is attractive for its simplicity, it’s not very flexible.

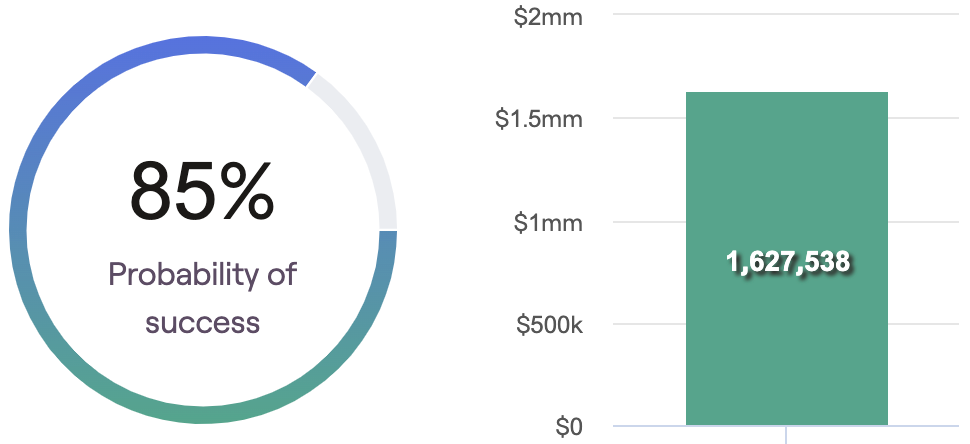

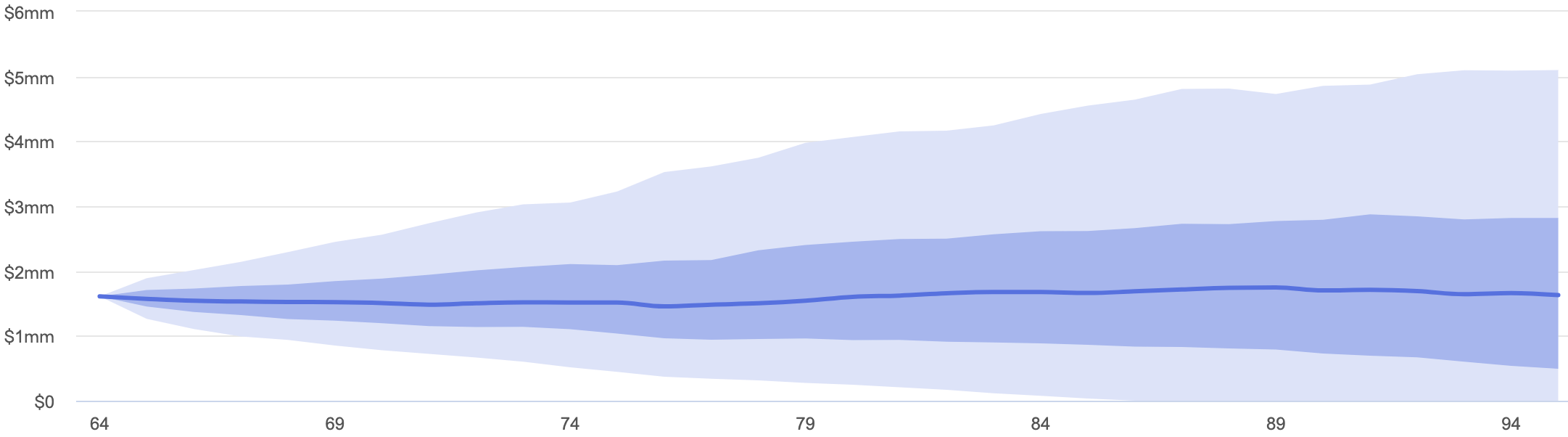

As you can see, this individual’s retirement income plan has an 85% “Probability of Success”. The projected end of plan median portfolio balance is $1,627,538. At age 86 years old the individual could potentially have $0 or over $4.6 mm. In our experience, having such a wide range of potential outcomes is not the most optimal way to plan for retirement income.

Source: RightCapital

In this article, we will discuss the guardrail approach, a dynamic strategy for retirement distributions that pivots away from “success or failure” to a framework for making adaptive adjustments.

The original guardrail framework was introduced to the financial planning industry after a research paper by Jonathan T. Guyton and William J. Klinger in the Journal of Financial Planning in March of 2006. It provided research on how calibrating your distributions based on how retirement unfolds could increase sustainable withdrawal rates.

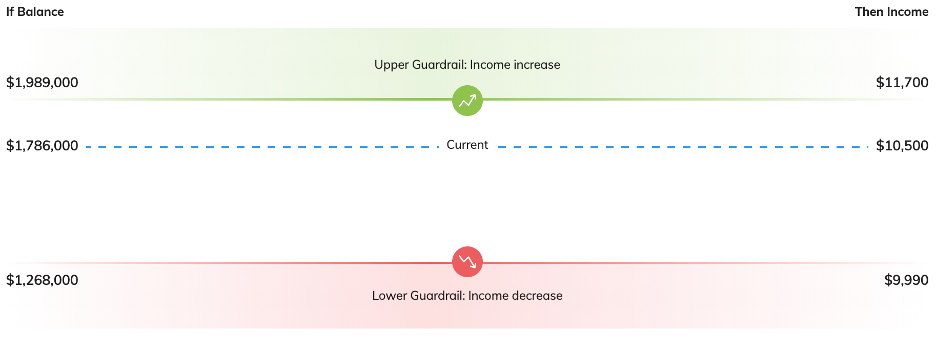

The risk-based guardrail strategy we currently use begins by specifying an initial monthly withdrawal amount. From here, two “guardrails” are established — one above and one below your current portfolio balance. These guardrails are designed to provide a framework for when adjustments to your income would be advised. If your investment conditions are better than anticipated, then your ability to spend increases. However, if these conditions deteriorate to certain point, then you have a lever to reduce spending until things improve.

Source: Income Lab

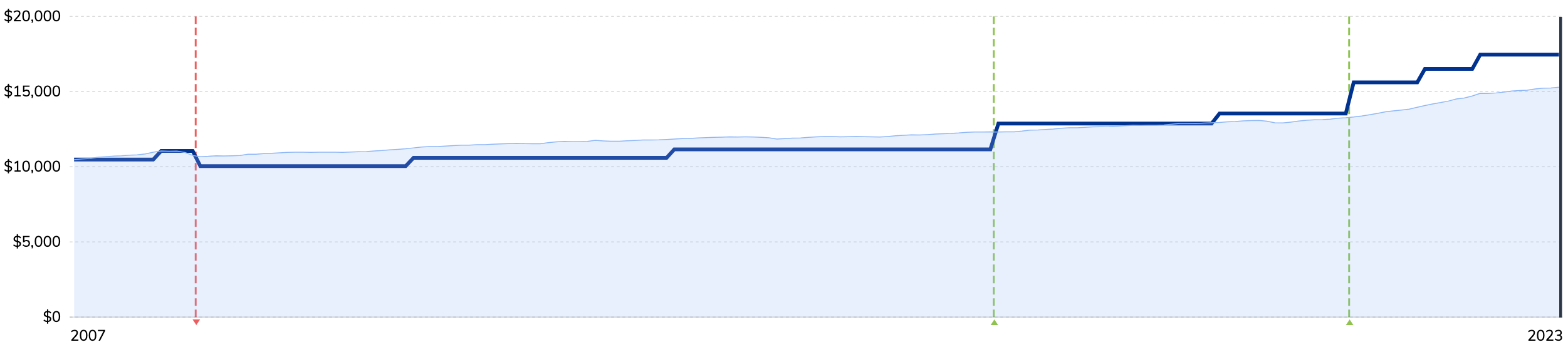

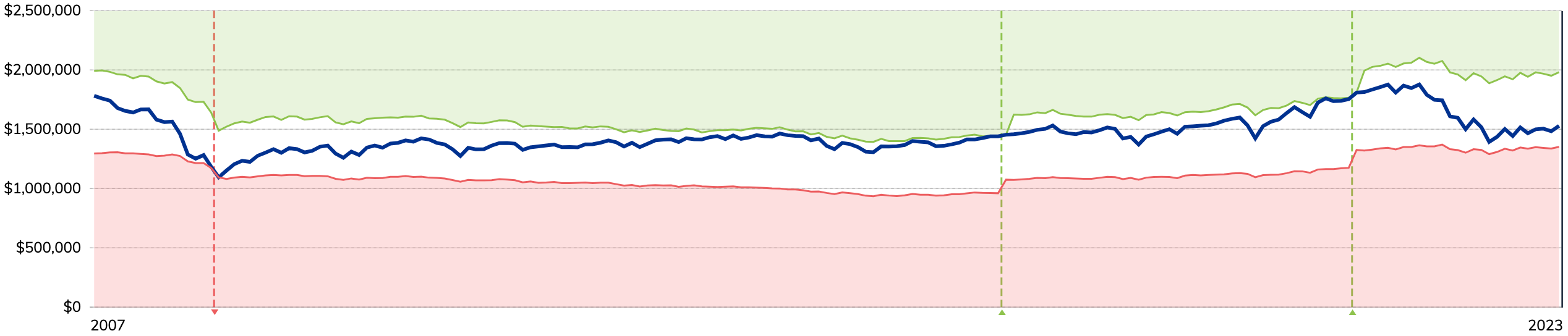

In this hypothetical scenario below, we look at an income plan during a period that experienced a global financial crisis, pandemic, high inflation, and four S&P 500 Index bear markets. The green dotted line represents upward income adjustments, while the red dotted line represents downward. As you can see, in favorable markets, withdrawals were increased, causing the portfolio balance to decrease. But when the portfolio hit the lower guardrail, withdrawals were cut back. Through this adaptive process, both the income and portfolio were guided through this challenging period.

Source: Income Lab

Source: Income Lab

While a guardrails retirement income strategy can be an attractive way to systematically adjust your retirement plan over time, it is not without some drawbacks. Let’s briefly review the major pros and cons of this strategy.

1. Flexibility and responsiveness to life changes.

Standard retirement approaches, which assume a fixed withdrawal rate, can struggle to accommodate a change in personal, health, financial or economic conditions. No one has a crystal ball on what the future holds so it is important to have a plan that is flexible and adaptive. The guardrail approach is specifically designed to account for these types of changes.

2. Psychological comfort.

For some retirees, it may be comforting to know that a plan is in place that accounts for shifts in the market. There is typically a tightening of spending when there is negative economic or market news. This adaptive framework can help to have clearly defined points at which a lifestyle adjustment may be necessary.

3. Potentially higher spending.

The guardrail framework provides steps that can reduce the risk of underspending throughout retirement. The risk of underspending is the regret that individuals can have at the tail end of retirement, when they look back and wish they would of retired earlier or spent more during their healthier years.

1. Complexity.

The guardrail approach requires you to frequently monitor your portfolio and perform calculations. This concern can be alleviated by working with a flat fee financial advisor or financial planner on implementation and monitoring of the strategy.

2. May result in income reductions.

Income reduction is often seen as the biggest drawback of the guardrail strategy. This is why it is critical that the guardrail strategy is part of a broader comprehensive financial plan that accounts for income required to cover your essential non-discretionary expenses.

3. Could result in a low ending portfolio balance.

While this isn’t necessarily a bad thing, since it would mean you maximized your retirement savings, many people want to leave behind a legacy for the next generation. Exhausting your portfolio could inhibit achieving this goal if you don’t establish a legacy goal as part of the guardrail framework.

Given the pros and cons we discussed, the guardrail approach may not be right for everyone. Let’s walk through some of the characteristics that could make this strategy a good fit for a retiree.

The guardrail approach may be more complex than other retirement strategies, but its flexibility, adaptability, and sustainability make it a compelling choice when compared to simpler approaches. And while it’s not easy to see your income dip during retirement, there is a psychological benefit to knowing that you have a framework to use that minimizes the risk of overspending or underspending throughout retirement.

If you’d like to speak with a flat fee financial advisor in Tampa about whether the guardrail approach is right for you, our team at Southshore Financial Planning is here to serve you.

Southshore Financial Planning LLC is a registered investment adviser offering services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This publication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This publication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made by the Author, in the future, will be profitable or equal the performance noted in this publication. All opinions and estimates constitute Southshore Financial Planning LLC’s judgment as of the date the information was printed and are subject to change without notice. Southshore Financial Planning LLC does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Southshore Financial Planning LLC be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if Southshore Financial Planning LLC or a Southshore Financial Planning LLC authorized representative has been advised of the possibility of such damages. The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Southshore Financial Planning LLC (referred to as “Southshore Financial Planning”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Federal tax advice disclaimer: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Southshore Financial Planning LLC to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Use of any information presented by Southshore Financial Planning LLC is for general information only and does not represent individualized tax advice, either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

Chris Shoup, CFP®

Founder, Financial Advisor

We deliver financial planning and investment management strategies that are personalized to your needs, goals and lifestyle.

Talk with an AdvisorOffice: 1600 E 8th Ave., Ste. A200 Tampa, FL 33605

Additional Meeting Location: 200 Central Ave. St. Petersburg, FL 33701

© Southshore Financial Planning. All Rights Reserved. Privacy Policy. Form ADV. Designed by Converting Attention.

Southshore Financial Planning LLC (“Southshore Financial Planning”, “Southshore”) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Southshore Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant to an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Southshore Financial Planning, unless otherwise specifically cited. Material presented is believed to be from reliable sources, and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.