As you enter your retirement years, life can change in a number of important ways. One of these changes might be the transition from an employer-sponsored health plan to Medicare, which is sponsored by the government. If you’re a high earner, however, you’ll need to watch out for an additional Medicare charge that catches many people by surprise.

IRMAA (Income-Related Monthly Adjustment Amount) surcharges are additional monthly premiums that high-income individuals and married couples must pay in addition to their regular Medicare charges. IRMAA impacts Medicare Part B and Part D, potentially leading to a sizable premium increase.

In certain cases, IRMAA surcharges can more than triple your Part B premiums. Moreover, in 2023 IRMAA can require an extra $76.40 per month on top of your standard Part D charges.

Because these extra payments can impact your financial plan, it’s vital to understand whether you’ll be subject to IRMAA surcharges. In this article, we’ll dive into the IRMAA technicalities, including ways in which you might be able to avoid paying extra. If you need additional guidance, a flat fee financial advisor can help you formulate a plan for your retirement years, including how to navigate IRMAA charges.

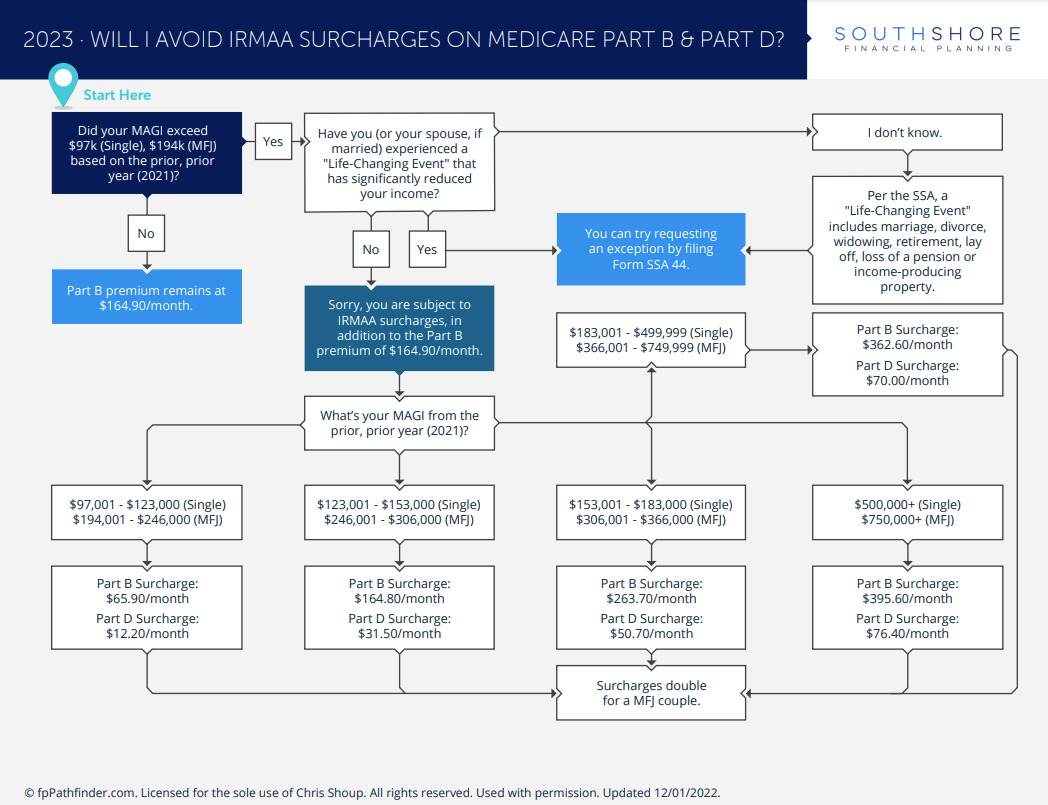

In a nutshell, if you earn more than $97,000 a year filing single or $194,000 a year filing jointly while using Medicare Part B or Part D, you will likely be impacted by IRMAA surcharges. The exact amount depends, however, on your Modified Adjusted Gross Income (MAGI). Below is a helpful flowchart that breaks down exact premiums based on income and filing status. You can download the flowchart here.

IRMAA charges increase Medicare Part B and Part D premiums. It’s important to note, however, that Medicare Advantage plans (also known as Medicare Part C) are also subject to IRMAA surcharges. This is because Medicare Advantage serves as an alternative way to receive Medicare Part B and Part D benefits.

Frustratingly for some, IRMAA is determined by your tax return information two years prior. This means that for your 2023 Medicare premium calculation, your 2021 tax return will be used. In certain instances, this gap means that IRMAA charges can be applied based on outdated information.

If you believe this is the case for you, it’s possible to file a redetermination request and have your IRMAA surcharges reduced or even eliminated. There are two ways to request a new determination, each of which requires you to show that your current income is not as high as initially determined.

If you’ve received a determination notice from the Social Security Administration (SSA) indicating that you will owe additional IRMAA premiums, it is possible to request a new determination, so long as you do so within 60 days of the initial notice.

You could take one of two approaches to request a review of a questionable determination.

The first is the straightforward case in which the SSA is using incorrect or outdated tax information. An inaccuracy could result from the SSA pulling information from a tax return that you later amended. Clerical errors are also possible. In the case that you have a more recent tax return showing a drop in income, you can use that return to request a reevaluation of your IRMAA status.

The second strategy has to do with what the SSA calls “life-changing events.” These events are significant changes in your circumstances that resulted in an income decrease. Currently, the SSA recognizes these eight events as life-changing:

If you can show that one of these events caused a significant drop in income, you might see your IRMAA surcharges adjusted. If your redetermination request does not come back with the answer you think is appropriate, you can appeal the decision.

If you are unable to successfully lower your IRMAA surcharges through a redetermination or an appeal, it’s still possible to lower future charges by reducing your taxable income.

Since the SSA determines IRMAA charges based on your MAGI, it’s possible to lower or even eliminate IRMAA charges by reducing your MAGI. Of course, it’s important to do this in an effective manner, since it wouldn’t make sense to simply lower your income by an amount greater than the IRMAA charges you need to pay.

One way to lower your MAGI is by donating money or investments to a qualified charity. Charitable donations reduce your taxable income, which can be an effective strategy to achieve philanthropic goals while lowering your IRMAA charges.

If you’d prefer to hang onto your money, you can contribute to a tax-deferred retirement plan or account. Contributions to traditional IRAs, 401(k)s, 403(b)s, and SEP IRAs reduce your taxable income for the year by the amount that you contribute, so long as the contribution amount does not exceed your earned income for the year or any contribution limits. If eligible, Health Savings Accounts (HSA) or Medical Savings Accounts (MSA) are also options to consider that can lower MAGI.

If you’re withdrawing money from an account, rather than contributing to it, you can still lower or reduce your IRMAA surcharges by using tax-efficient strategies. For instance, if you are selling assets in a taxable account to withdraw money, consider selling assets with a capital loss. Capital losses could lower your MAGI by offsetting capital gains or other income. Alternatively, if you have an account that are subject to future Required Minimum Distributions (RMDs), you might want to consider Roth IRA conversions or increase withdrawals during low-income years, so that large RMDs will not push you into a higher IRMAA bracket during high-income years.

Understanding, navigating, and possibly avoiding IRMAA charges can be a challenge. One way to ensure you’re taking the optimal path forward is by working with a flat fee financial planner in the Tampa Bay area.

At Southshore Financial Planning, we strive to help our clients understand their finances with a comprehensive plan. Reach out to our team today to discuss IRMAA charges or any other aspects of your financial life we can assist you with.

Southshore Financial Planning LLC is a registered investment adviser offering services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This publication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This publication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made by the Author, in the future, will be profitable or equal the performance noted in this publication. All opinions and estimates constitute Southshore Financial Planning LLC’s judgment as of the date the information was printed and are subject to change without notice. Southshore Financial Planning LLC does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Southshore Financial Planning LLC be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if Southshore Financial Planning LLC or a Southshore Financial Planning LLC authorized representative has been advised of the possibility of such damages. The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Southshore Financial Planning LLC (referred to as “Southshore Financial Planning”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Federal tax advice disclaimer: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Southshore Financial Planning LLC to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Use of any information presented by Southshore Financial Planning LLC is for general information only and does not represent individualized tax advice, either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

Chris Shoup, CFP®

Founder, Financial Advisor

We deliver financial planning and investment management strategies that are personalized to your needs, goals and lifestyle.

Talk with an AdvisorOffice: 1600 E 8th Ave., Ste. A200 Tampa, FL 33605

Additional Meeting Location: 200 Central Ave. St. Petersburg, FL 33701

© Southshore Financial Planning. All Rights Reserved. Privacy Policy. Form ADV. Designed by Converting Attention.

Southshore Financial Planning LLC (“Southshore Financial Planning”, “Southshore”) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Southshore Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant to an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Southshore Financial Planning, unless otherwise specifically cited. Material presented is believed to be from reliable sources, and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.