The DIY Retirement Trap: 5 Blind Spots Retirees Often Overlook

Retiring in the Sunshine State is a dream decades in the making. Whether you’re eyeing a golf course villa in Lakewood Ranch or a quiet coastal retreat on Clearwater Beach, the transition from "saving mode" to "spending mode" is the most complex financial shift you’ll ever make.

Many disciplined Floridians have successfully managed their own portfolios during their working years. However, retirement planning is not the same as investment management. When you stop receiving a paycheck, the rules of the game change. The strategies that grew your wealth are often the very ones that can jeopardize it during distribution.

At Southshore Financial Planning, we see many "Do-It-Yourself" (DIY) investors who are brilliant at accumulating assets but struggle with the nuances of retirement. Here are the top five critical areas DIYers often miss when crafting their own Florida retirement roadmap.

1. The Myth of "Set and Forget" Asset Allocation

Most DIY investors understand that they need a mix of stocks and bonds. However, they often fail to adjust that allocation to mitigate the Sequence of Returns Risk.

In your 40s, a 20% market dip is a "buying opportunity." In your first year of retirement, a 20% dip combined with your monthly withdrawals could jeopardize the longevity of your next egg. This is because you are selling shares at a loss to fund your lifestyle, leaving fewer shares behind to participate in the eventual recovery.

DIY Risk: Many retirees here hold onto aggressive growth stocks because they want to "keep up" with inflation or have had great equity returns over the past year. Without a dedicated "buffer" or "bucket" of liquid, low-volatility assets to cover 2–3 years of spending, they may be forced to sell positions that have pulled back dramatically during a market downturn.

Strategy Shift: Instead of just a static mix of stocks and bonds, consider a hybrid approach that incorporates elements of a Liability-Driven Investment (LDI) strategy within a broader asset allocation. This means matching specific cash-flow needs over the next few years with safe assets while letting higher-risk investments ride out volatility.

2. The "Umbrella" Hole in Your Liability Coverage

Anyone who has driven even ten miles on I-75, US-19, or the Selmon Express knows the landscape of Florida highways is defined by one thing: a sea of towering billboards featuring personal injury attorneys.

Florida is a litigious state, and high-net-worth retirees can be seen as "deep pockets." DIYers are usually great at finding the best rates on homeowners or auto insurance, but they frequently overlook adding a Personal Liability Umbrella Insurance (PLUP).

If you are involved in a multi-car accident on I-75 or if a guest is injured at your pool, your standard $300,000 auto or home liability limit can be exhausted in minutes. In Florida, your retirement accounts (such as 401 (k) s and IRAs) have significant protections from creditors. Still, your brokerage accounts, real estate (beyond your homestead), and future income may be at risk.

DIY Risk: It’s not an "investment," so it doesn't show up on a brokerage statement. Yet, an umbrella policy is one of the most cost-effective ways to protect your retirement nest egg.

Strategy Shift: For a few hundred dollars a year, an umbrella policy provides an extra layer of defense that ensures a single legal judgment doesn't force you to decrease your retirement spending dramatically.

3. Ignoring the "Retirement Spending Smile"

One of the most common DIY mistakes is projecting retirement spending as a straight line adjusted for inflation (e.g., "I need $12,000 a month every month for 30 years"). Real life doesn't work that way.

Research attributed to David Blanchett in his paper, Exploring the Retirement Consumption Puzzle, shows that retirement spending typically follows a "Spending Smile", often categorized into three phases:

- The Go-Go Years: This is when spending is highest. You’re healthy, traveling, joining social clubs, and finally tackling bucket list items.

- The Slow-Go Years: Activity slows down. You might travel less and share a meal when dining out. Discretionary spending naturally dips.

- The No-Go Years: Spending often spikes again, but it’s no longer for fun. Healthcare costs, in-home care, assisted living, or nursing home dominate this phase.

DIY Risk: Over-funding the "Go-Go" years without accounting for the late-stage healthcare spike, or under-spending in early retirement out of fear, you miss the window of vitality that you worked so hard to reach.

Strategy Shift: Create a cash flow plan that incorporates phased spending shifts to balance the enjoyment of retirement with the need to ensure the portfolio lasts.

4. Recency Bias and Investment Concentration

It’s human nature: we want to own more of what performed well last year. DIYers often fall into the trap of Investment Concentration, particularly in "hot" sectors or the single best-performing fund or stock in their portfolio from the previous 12 months.

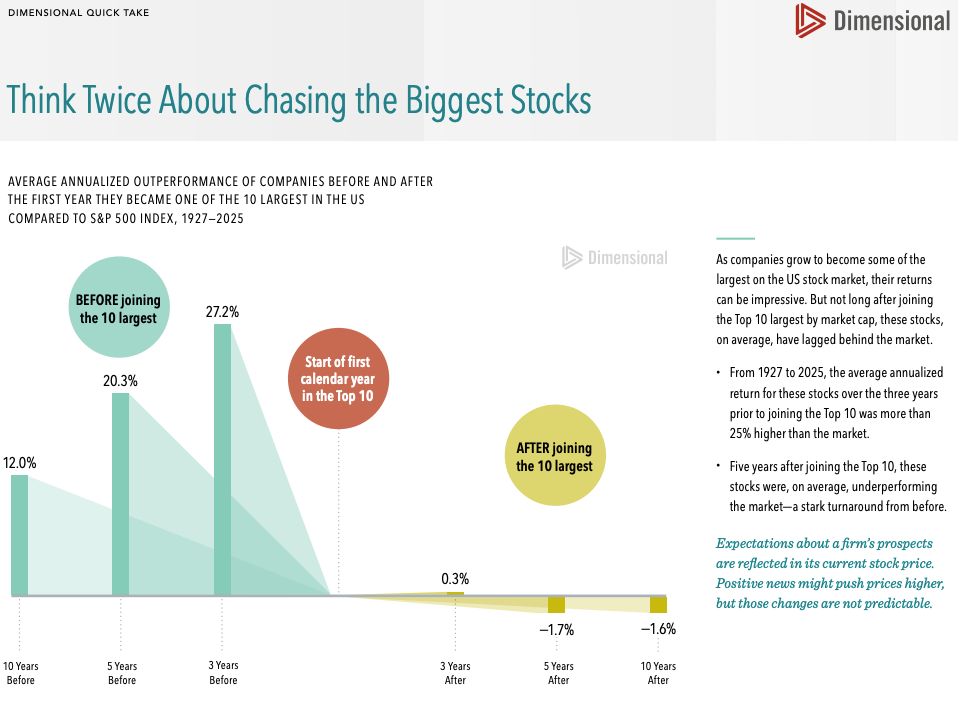

Here is an illustration of a company's performance before and after reaching the “Top 10” status from 1927-2025

Source: Dimensional Fund Advisors

In Florida, we often see this with retirees who became overweight in Tech or in specific S&P 500 winners. While it felt great in 2023 and 2024, only two of the “Magnificent 7” stocks outperformed the S&P 500 index in 2025.

DIY Risk: Seeing an investment way up and deciding to "let it ride."

Strategy Shift: "Trimming the trees"—taking the gains from the winners to replenish the safer side of the portfolio or liquidity “bucket”. This forced discipline of "selling high" is something most find emotionally difficult to follow through on on their own.

5. Relying on a "Rule of Thumb" (The 4% Rule)

For decades, the "4% Rule" has been the holy grail of DIY retirement. The math was simple: withdraw 4% of your portfolio in year one, adjust that dollar amount for inflation every year thereafter, and your money would likely last 30 years.

However, relying on this as a rigid "rule" is one of the most common—and potentially costly—mistakes we see in Florida retirement plans.

The Origin Story: It Was Never a "Rule"

The concept was pioneered in 1994 by William Bengen, an MIT-educated rocket scientist turned financial planner. Interestingly, Bengen never intended for 4% to be a universal law. His original research, published in the Journal of Financial Planning, actually calculated a "safe" withdrawal rate of 4.15%, but it was rounded down to 4% for simplicity in professional journals—and the name stuck.

Bengen called this number the "SAFEMAX"—the maximum amount you could have withdrawn in the absolute worst economic period in U.S. history (specifically, retiring in October 1968, just before a decade of stagflation). For the "average" retiree, the 4% rule is actually quite conservative.

The Evolution: From 4% to 4.7% and Beyond

Just as Florida’s landscape has changed since the 90s, so has Bengen's thinking. In his 2025 book, A Richer Retirement, Bengen updated his research to reflect a more modern, diversified portfolio. By including asset classes such as small-cap stocks and international equities—which weren't included in his original 1994 study—he has raised his "safe" baseline to 4.7%.

Recently, he has advocated for a more nuanced approach, noting that a rigid 4% withdrawal often leads to the "Spend-Down Paradox": retirees live too frugally in their best years, only to leave a massive, unspent surplus to heirs who didn't do the work to save it.

The Better Way: Risk-Based Guardrails

If the 4% rule is too rigid, what’s the alternative? At Southshore Financial Planning, we utilize a Risk-Based Guardrail Approach.

Think of guardrails like the ones on the Sunshine Skyway Bridge: they are there to keep you on the road, but they don't force you to drive in a single, narrow lane. This approach balances two primary risks:

- The Risk of Overspending: If the market tanks, the guardrails tell you exactly when and how much to trim your spending to preserve your capital.

- The Risk of Underspending: If the market booms, the guardrails give you a "prosperity raise," allowing you to spend more on that extra travel or family legacy while you're still healthy enough to enjoy it.

Why Guardrails Win for Florida Retirees

Unlike a static rule, a guardrail strategy is dynamic. It calculates your withdrawal as a percentage of your current portfolio value, not just your starting balance from years ago.

- The Prosperity Rule: If your portfolio grows so much that your withdrawal rate drops significantly, you take a raise.

- The Capital Preservation Rule: If a market downturn pushes your withdrawal rate above a target, you reduce spending.

This flexibility allows many of our clients to start with an initial withdrawal rate significantly higher than the old 4% rule, because they have a disciplined system in place to adjust if the weather gets rough.

Transitioning from Manager to Retiree

Being a DIY investor can be a badge of honor, but the stakes change when "Return ON Capital" becomes less important than "Return OF Capital." Missing even one of these five areas—asset allocation, liability protection, spending phases, concentration risk, or withdrawal logic—can lead to unnecessary stress during your best years.

At Southshore Financial Planning, we meet families exactly where they are—whether you need a one-time, comprehensive retirement plan to validate your DIY strategy or ongoing wealth management to navigate the decades of distribution ahead. We don’t just manage accounts; we architect the structural framework for your future, ensuring your plan stays as resilient as a Florida home in a storm.

Which Path Fits Your Situation?

We recognize that not every retiree wants—or needs—the same level of engagement. Our goal is to provide the expertise you lack, not to take over the things you enjoy doing yourself.

- The One-Time SFP Retirement Plan: Perfect for the disciplined DIYer who wants a professional "second opinion" or a forensic stress test. We build the plan, set your guardrails, and hand you the keys to execute it with confidence.

- Ongoing Wealth Management: For those who want a dedicated co-pilot. We provide continuous monitoring, tax planning, investment management, and tax-efficient withdrawal execution, allowing you to spend your time on the golf course or with family rather than watching ticker symbols.

Whether you're looking for a one-time "GPS calibration" for your nest egg or a long-term partner to navigate the market's shifting tides, we provide the clarity needed to turn your savings into a sustainable lifestyle.